1. What is the Asia Pacific Food Service Packaging Market overview, including its definition, scope, and significance?

The Asia Pacific Food Service Packaging Market comprises all packaging solutions used by restaurants, catering services, and food‑service outlets across the Asia‑Pacific region. It covers materials such as plastic and metal, applications ranging from beverages to bakery items, and both flexible and rigid packaging types. The market is significant because it enables hygiene, extends shelf life, supports convenience trends, and underpins the rapid growth of food‑service outlets in emerging economies.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Asia Pacific Food Service Packaging Market?

Key drivers include rising disposable income, urbanisation, and the booming food‑service sector, which boost demand for safe and convenient packaging. Environmental regulations and consumer demand for sustainable solutions present both a restraint and an opportunity, prompting innovation in recyclable plastics and metal alternatives. Challenges stem from fluctuating raw‑material costs and fragmented supply chains. Opportunities arise from e‑commerce food delivery growth and advances in biodegradable packaging technologies.

3. Which growth trends are currently influencing the Asia Pacific Food Service Packaging Market?

Current trends feature a shift toward lightweight, high‑barrier flexible films, increased adoption of metal‑based containers for premium beverages, and the integration of smart packaging for traceability. The market also sees a surge in plant‑based and compostable plastics, driven by sustainability mandates. Moreover, the rise of cloud kitchens and ghost‑restaurant models is accelerating demand for durable, tamper‑evident packaging.

4. How has COVID‑19 impacted the Asia Pacific Food Service Packaging Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced on‑premise dining, leading to a temporary dip in packaging volumes. However, the rapid expansion of take‑out, delivery, and curb‑side services created a surge in demand for single‑use packaging. Recovery is now robust, with market confidence restored as vaccination rates rise and consumer preference for contact‑less food consumption remains strong.

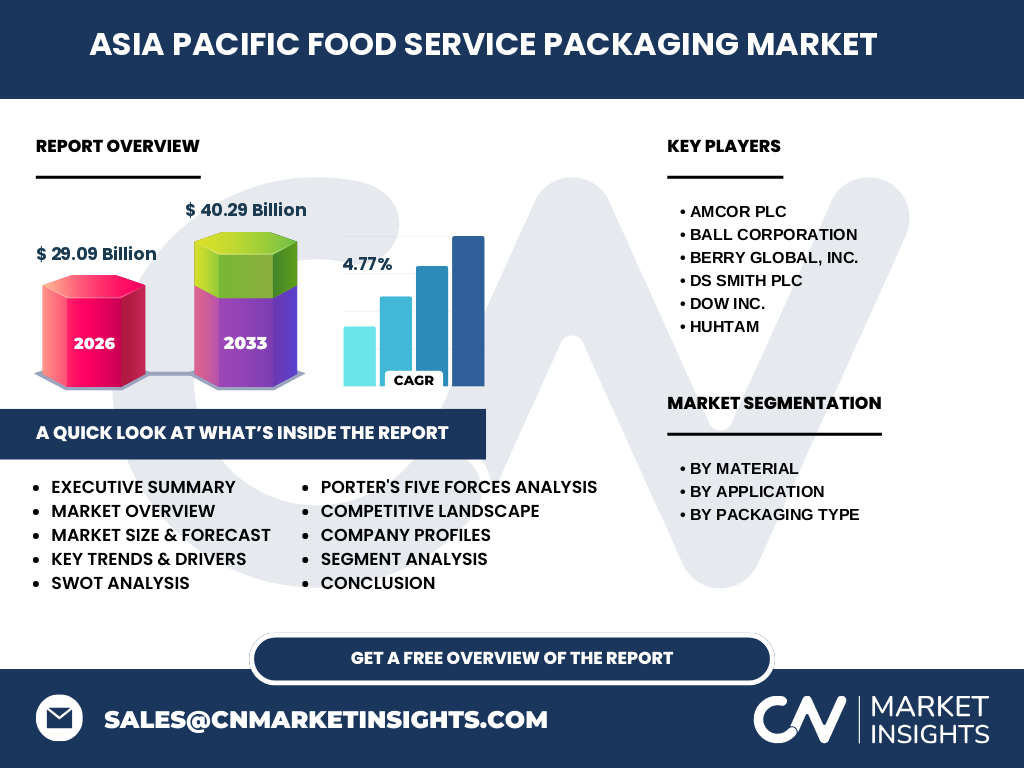

5. Who are the major competitors in the Asia Pacific Food Service Packaging Market, and what is the level of market consolidation?

Leading players include Amcor plc, Ball Corporation, Berry Global, Inc., DS Smith PLC, Dow Inc., and Huhtam. These firms compete on material innovation, global distribution networks, and strategic acquisitions. The market shows moderate consolidation, with large multinational corporations acquiring niche regional manufacturers to broaden product portfolios and strengthen footholds in high‑growth countries such as China, India, and Indonesia.

6. What are the key findings highlighted in the executive summary of the Asia Pacific Food Service Packaging Market?

The market is projected to reach $40.29 billion by 2033, growing at a 4.77 % CAGR from a 2026 base of $29.09 billion. Plastic remains the dominant material, while metal gains traction in premium beverage segments. Flexible packaging leads in volume, driven by convenience and sustainability trends. Competitive dynamics are shaped by innovation in recyclable materials and strategic partnerships aimed at expanding e‑food‑service channels.

7. What are the forecast expectations for the Asia Pacific Food Service Packaging Market from 2025 to 2032?

Based on a 4.77 % CAGR, the market is expected to expand steadily, reaching approximately $40 billion by the early 2030s. Growth will be powered by continued urbanisation, higher food‑service penetration, and regulatory incentives for eco‑friendly packaging. Seasonal spikes are anticipated around major festivals in China, India, and Southeast Asia, further reinforcing demand cycles.

8. How is the market sized and shared by segmentation, such as material, application, and packaging type?

Segmentation by material splits primarily between plastic and metal, with plastic holding the larger share due to its versatility. Application‑wise, beverages and bakery/confectionery lead usage, followed by fruits & vegetables and dairy products. In terms of packaging type, flexible formats dominate because of their lightweight and cost‑effective nature, while rigid containers are preferred for premium and long‑shelf‑life items.

9. What is the geographic distribution of the Asia Pacific Food Service Packaging Market?

Geographically, the market is concentrated in East Asia (China, Japan, South Korea), Southeast Asia (Indonesia, Malaysia, Thailand, Vietnam), and South Asia (India). These sub‑regions collectively account for the majority of the $29.09 billion 2026 market size, reflecting strong food‑service growth, expanding middle‑class populations, and increasing retail‑outlet density.

10. How does each region within Asia Pacific perform in the food service packaging market?

China leads with the highest absolute volume, driven by its massive food‑service footprint and rapid e‑delivery expansion. India follows, benefitting from a youthful population and rising disposable income. Southeast Asian markets, particularly Indonesia and Vietnam, show the fastest growth rates due to urban migration and the proliferation of quick‑service restaurants. Japan and South Korea maintain steady demand, focusing on high‑quality, premium packaging.

11. Which companies are leading in the Asia Pacific Food Service Packaging Market, and what strategies are they employing?

Amcor plc focuses on sustainable solutions, expanding its recyclable plastic portfolio. Ball Corporation invests in aluminum can technology for beverage packaging. Berry Global emphasizes flexible film innovations. DS Smith pursues circular economy initiatives, while Dow Inc. leverages its polymer expertise for high‑performance barriers. Huhtam strengthens its market position through acquisitions of regional converters and product‑line extensions.

12. What does Porter’s Five Forces analysis reveal about the competitive environment of the Asia Pacific Food Service Packaging Market?

Buyer power is moderate, as large food‑service chains demand consistent quality and volume. Supplier power is high due to dependence on petrochemical feedstocks for plastic and metal ore prices. Threat of new entrants is limited by capital intensity and regulatory compliance costs. Substitutes, such as reusable containers, pose a growing threat. Competitive rivalry is intense, driven by product differentiation and cost efficiencies.

13. What are the SWOT highlights for the Asia Pacific Food Service Packaging Market?

Strengths: Large and growing food‑service base, diversified material options, and strong logistics networks.

Weaknesses: Vulnerability to raw‑material price volatility and environmental criticism of single‑use plastics.

Opportunities: Expansion of sustainable packaging, digital printing for customization, and penetration of remote‑rural markets.

Threats: Stricter regulatory bans on non‑recyclable plastics and rising competition from local manufacturers.

14. How is the value chain structured for the Asia Pacific Food Service Packaging Market?

The value chain starts with raw‑material suppliers (petrochemical plants, metal mills), followed by polymer and metal processing firms. These feed packaging converters that produce flexible films, rigid containers, and composite solutions. Distributors and logistics providers then deliver finished packaging to food‑service operators, while end‑users—restaurants, cafes, and delivery platforms—generate demand. Recycling and waste‑management services close the loop.

15. What key investment insights can be drawn for stakeholders interested in the Asia Pacific Food Service Packaging Market?

Investors should prioritize companies with strong sustainability pipelines and capabilities in recyclable plastics or lightweight metal packaging. Strategic partnerships with e‑food‑service platforms can accelerate market entry. Funding R&D in biodegradable materials offers long‑term differentiation, while acquiring regional converters provides immediate access to high‑growth markets such as India and Southeast Asia.

16. What are the main conclusions and takeaways from the Asia Pacific Food Service Packaging Market analysis?

The market is on a steady growth trajectory, expected to surpass $40 billion by 2033. Plastic remains dominant, yet metal and sustainable alternatives are gaining ground. Flexible packaging leads due to cost and convenience, while regional demand is led by China, India, and Southeast Asia. Competitive dynamics revolve around innovation, regulatory compliance, and strategic acquisitions.

17. What research methodology was applied to develop this market report?

The study combined primary interviews with industry experts, secondary data from company filings, trade publications, and government statistics. Quantitative analysis employed trend extrapolation based on the provided 2026 market size ($29.09 billion) and the forecast figure ($40.29 billion), deriving a CAGR of 4.77 %. Segmentations were validated through cross‑referencing multiple sources.

18. What is the scope of this research, and what limitations should readers be aware of?

The scope covers material, application, and packaging‑type segmentation for the Asia Pacific region, focusing on major economies and leading players. Limitations include the exclusion of granular country‑level financial breakdowns and the reliance on publicly available data; proprietary or confidential figures were not incorporated.

19. Which key companies have recent developments in the Asia Pacific Food Service Packaging Market?

Amcor plc announced a new line of recyclable flexible films for beverage carriers. Ball Corporation launched a high‑strength aluminum can series targeting premium coffee drinks. Berry Global introduced compostable stretch films for bakery items. DS Smith reported a joint venture with an Indonesian converter to expand rigid packaging capacity. Dow Inc. unveiled a polymer blend that enhances barrier performance for dairy applications. Huhtam completed the acquisition of a Thai flexible‑pack manufacturer, strengthening its foothold in Southeast Asia.